Unemployment

The unemployment level was stable or slightly growing in December 2014, depending on the methodology used. 5.9% of the active population was unemployed, or 7.4% of the total population. The hopes were for better data. It is certainly true that the unemployment level decreased by about 1% in 2014, but the GDP grew by about 2%. Furthermore, strong policies were implemented to support exports, such as the forced undervaluation of the crown, which were expected to generate more permanent jobs. The fact is that Prague and its region is always in a de facto full employment state, whereas the economy in large parts of the country remain in a chronic state of economic depression, without any sign of improvement. For instance, the Ostrava region, and the north of Bohemia. There unfortunately the active population, when unemployed, is quite averse to moving to areas with more job opportunities. Many prefer unemployment subsidized by a welfare that is very generous for the regions where the cost of living is low, but quite insufficient in the most developed areas.

The unemployment level was stable or slightly growing in December 2014, depending on the methodology used. 5.9% of the active population was unemployed, or 7.4% of the total population. The hopes were for better data. It is certainly true that the unemployment level decreased by about 1% in 2014, but the GDP grew by about 2%. Furthermore, strong policies were implemented to support exports, such as the forced undervaluation of the crown, which were expected to generate more permanent jobs. The fact is that Prague and its region is always in a de facto full employment state, whereas the economy in large parts of the country remain in a chronic state of economic depression, without any sign of improvement. For instance, the Ostrava region, and the north of Bohemia. There unfortunately the active population, when unemployed, is quite averse to moving to areas with more job opportunities. Many prefer unemployment subsidized by a welfare that is very generous for the regions where the cost of living is low, but quite insufficient in the most developed areas.

Industrial production

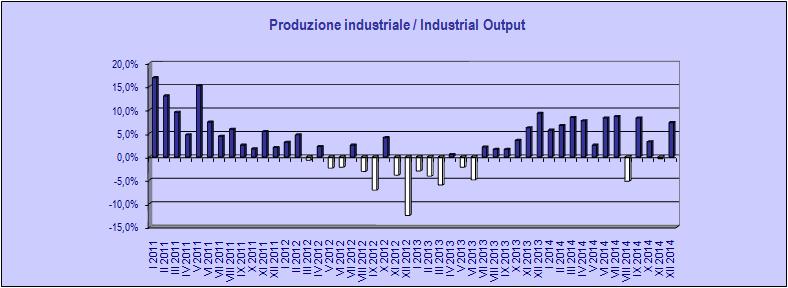

The industrial production recorded a nice +7.3% increase y-on-y. As usual, the automotive sector was carrying the Czech industry, growing by 16%. For the entire year 2014 the industrial output increased by 4.9%, a very strong figure that helped the GDP grow by about 2.3%. In comparison to neighbouring countries, and the Eurozone, those are staggering figures. In December, the industrial output for the Eurozone was flat, and for the whole of 2014 the growth was a mere 0.6%. There are several reasons for the excellent Czech performance. The forced undervaluation of the crown certainly helped, as did the fairly low salary level in manufacturing, though slightly increasing. The expectations are quite positive, since the new orders were also growing, by 12% in December. The hopes are that this positive climate will determine the creation of more new permanent jobs.

The industrial production recorded a nice +7.3% increase y-on-y. As usual, the automotive sector was carrying the Czech industry, growing by 16%. For the entire year 2014 the industrial output increased by 4.9%, a very strong figure that helped the GDP grow by about 2.3%. In comparison to neighbouring countries, and the Eurozone, those are staggering figures. In December, the industrial output for the Eurozone was flat, and for the whole of 2014 the growth was a mere 0.6%. There are several reasons for the excellent Czech performance. The forced undervaluation of the crown certainly helped, as did the fairly low salary level in manufacturing, though slightly increasing. The expectations are quite positive, since the new orders were also growing, by 12% in December. The hopes are that this positive climate will determine the creation of more new permanent jobs.

Inflation

The Data for January confirm that the Czech economy is in a de facto deflationary state. Notwithstanding excellent performances in industrial output and foreign trade, and the artificially undervalued exchange rate, there are no signs of an exit from such a harmful situation for the economy. In January the CPI increase was 0.1%, and for the whole of 2014 it was only 0.3% on average. Unfortunately, for the Czech Republic, the economic system is not big enough to counteract the deflation imported from the Eurozone. It eventually seemed that ECB realized that the reality was so far off its statutory target of 2%, and will maybe finally implement some form of QE, which nowadays everybody knows is necessary. Meanwhile, prices keep falling, reducing the sentiment towards investing, as is domestic demand and the creation of new permanent jobs. There are those benefit from this situation, albeit just temporarily. Those who hold savings, preferably in dollars, and are willing to buy durable goods. For everybody else, that is the majority the outlook is rather negative.

The Data for January confirm that the Czech economy is in a de facto deflationary state. Notwithstanding excellent performances in industrial output and foreign trade, and the artificially undervalued exchange rate, there are no signs of an exit from such a harmful situation for the economy. In January the CPI increase was 0.1%, and for the whole of 2014 it was only 0.3% on average. Unfortunately, for the Czech Republic, the economic system is not big enough to counteract the deflation imported from the Eurozone. It eventually seemed that ECB realized that the reality was so far off its statutory target of 2%, and will maybe finally implement some form of QE, which nowadays everybody knows is necessary. Meanwhile, prices keep falling, reducing the sentiment towards investing, as is domestic demand and the creation of new permanent jobs. There are those benefit from this situation, albeit just temporarily. Those who hold savings, preferably in dollars, and are willing to buy durable goods. For everybody else, that is the majority the outlook is rather negative.

Foreign Trade

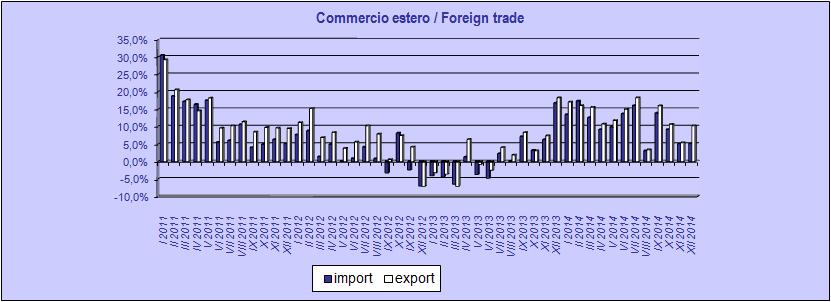

In the year 2014 the Czech Republic proved itself once again to be a very strong exporter. Exports grew by 13.5% when compared to 2013, thanks also to the nice December performance that showed a 10.3% increase, versus a 5.1% increase of imports, the latter was certainly helped by the cheap price of oil. Imports in 2013 grew by 11.8%. The bottom line, is the trade balance for that year was in deep positive territory, at 157bn Crowns. That, when compared to 2013, fared better by 50bn, by about 32%. Obviously, this performance put strong pressure on the appreciation of the Czech Crown. The ČNB kept fighting it with several tools, keeping the target exchange rate of 27 towards the Euro. Yet after the Swiss national bank gave up on the Franc-Euro peg, many wonder if the ČNB will end up exhausting its means and shall allow the CZK to fluctuate freely, since today it is heavily undervalued.

In the year 2014 the Czech Republic proved itself once again to be a very strong exporter. Exports grew by 13.5% when compared to 2013, thanks also to the nice December performance that showed a 10.3% increase, versus a 5.1% increase of imports, the latter was certainly helped by the cheap price of oil. Imports in 2013 grew by 11.8%. The bottom line, is the trade balance for that year was in deep positive territory, at 157bn Crowns. That, when compared to 2013, fared better by 50bn, by about 32%. Obviously, this performance put strong pressure on the appreciation of the Czech Crown. The ČNB kept fighting it with several tools, keeping the target exchange rate of 27 towards the Euro. Yet after the Swiss national bank gave up on the Franc-Euro peg, many wonder if the ČNB will end up exhausting its means and shall allow the CZK to fluctuate freely, since today it is heavily undervalued.

by Gianluca Zago